When exploring different loan options, you may come across the term balloon loan. While this type of financing can offer lower monthly payments in the short term, it comes with a unique structure that every borrower should fully understand. So, what is a balloon loan, and is it right for your financial situation?

This detailed guide will break down the definition, pros and cons, examples, and when it makes sense to consider a balloon loan—ensuring you have all the information needed to make an informed financial decision.

Definition: What Is a Balloon Loan?

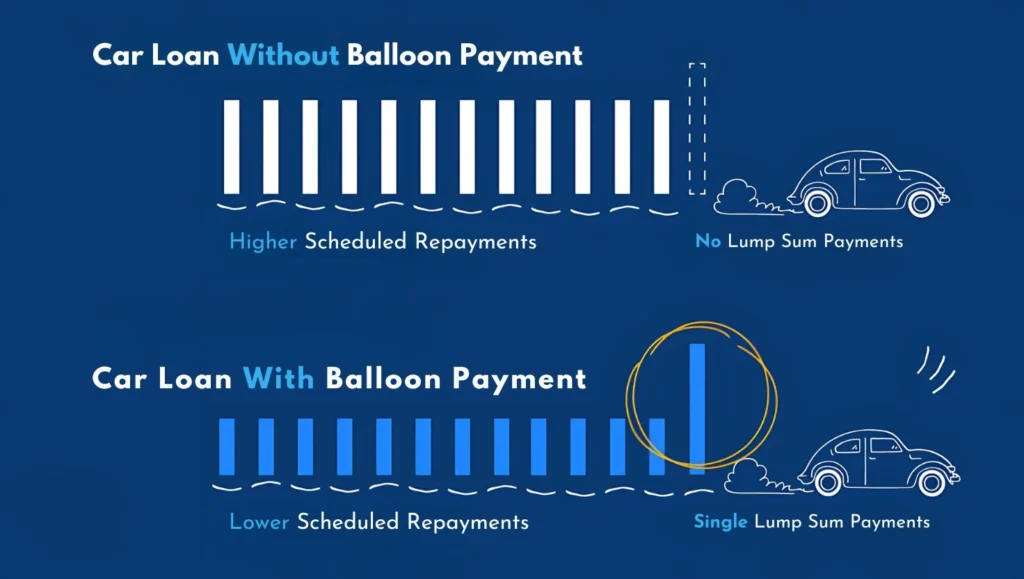

A balloon loan is a type of loan that does not fully amortize over its term. This means that instead of paying off the loan with regular monthly installments over time, the borrower makes smaller monthly payments, followed by a large lump-sum payment—known as the balloon payment—at the end of the loan term.

This final payment can be significantly larger than the earlier payments and typically represents the remaining balance of the loan principal.

How a Balloon Loan Works

With most loans, your monthly payments cover both principal and interest, gradually reducing the loan balance to zero by the end of the term. However, with a balloon loan:

- You make low or interest-only payments during the initial term (e.g., 5 or 7 years).

- At the end of the term, you owe a large final payment—the “balloon”—to pay off the remaining loan balance.

- The balloon payment is often tens of thousands of dollars, depending on the original loan amount and term.

Balloon loans are commonly used in real estate, commercial lending, and auto financing, though they are less common in standard consumer loans.

Example of a Balloon Loan

Let’s say you borrow $100,000 with a 5-year balloon loan at 5% interest:

- You agree to monthly payments of interest only, which equals $416.67 per month.

- After 60 months (5 years), you will have paid $25,000 in interest.

- At the end of the 5-year term, you still owe the entire $100,000 as a balloon payment.

Alternatively, some balloon loans require partial amortization, where your monthly payments include a portion of the principal. Even then, the final payment remains large.

Key Features of Balloon Loans

- Short-term structure: Common terms range from 3 to 7 years.

- Lower initial payments: Due to interest-only or partial amortization.

- Large final payment: The balloon payment at the end of the loan.

- Refinancing or selling often required: Most borrowers cannot afford the final lump sum without refinancing or liquidating an asset.

Advantages of Balloon Loans

1. Lower Monthly Payments

Since you’re only paying interest or a small portion of the principal, balloon loans offer affordable monthly payments during the loan term.

2. Useful for Short-Term Needs

Balloon loans are ideal for those who plan to sell or refinance before the balloon payment is due—such as businesses with short-term cash flow needs or property investors.

3. Flexible Use of Capital

Lower payments free up cash flow for other investments or business operations.

Disadvantages of Balloon Loans

1. Large Final Payment Risk

The balloon payment can be financially overwhelming if you don’t plan ahead or your financial situation changes.

2. Refinancing Isn’t Guaranteed

If your credit worsens or interest rates rise, refinancing the balloon payment may not be possible or affordable.

3. Potential for Default

If you can’t make the balloon payment or refinance, you risk defaulting on the loan and losing the asset (e.g., your home or car).

4. Higher Long-Term Cost

If you end up refinancing or extending the loan, you may pay more in interest over time.

When a Balloon Loan Makes Sense

A balloon loan may be a strategic choice under certain conditions:

- You plan to sell the asset (like real estate or a vehicle) before the balloon payment is due.

- You expect a significant increase in income or a financial windfall in the near future.

- You want to invest freed-up capital elsewhere during the initial loan term.

- You understand and accept the risk of refinancing later under uncertain market conditions.

Balloon Loan vs. Traditional Loan

| Feature | Balloon Loan | Traditional Loan |

|---|---|---|

| Monthly Payments | Lower (interest-only or partial) | Higher (full principal & interest) |

| Loan Term | Short (3–7 years) | Longer (15–30 years typical) |

| Final Payment | Large balloon payment | None (loan is fully paid off) |

| Risk Level | Higher due to refinancing/sale need | Lower with predictable payments |

| Ideal For | Short-term financing, investors | Long-term homeowners, stable income |

How to Prepare for a Balloon Payment

If you take out a balloon loan, here’s how to ensure you’re ready for the final lump-sum:

1. Understand the Total Balloon Amount

Know exactly how much you’ll owe and when.

2. Plan an Exit Strategy

Options include:

- Refinancing into a standard loan

- Selling the asset

- Paying in full with savings or other funding

3. Monitor Market Conditions

Refinancing is easier when interest rates are low and your credit score is high.

4. Build a Repayment Fund

Set aside money regularly to build a balloon payment reserve over time.

Where Balloon Loans Are Commonly Used

- Commercial Real Estate Financing: Investors plan to sell or refinance properties after appreciation.

- Auto Financing: Some car loans offer balloon options to reduce monthly payments.

- Business Loans: Used when short-term capital is needed, and future revenue is expected to cover the balloon.

- Construction or Bridge Loans: Designed for temporary funding until permanent financing is arranged.

Are Balloon Loans Safe?

Balloon loans can be safe if you have a clear repayment strategy and understand the risks. They are not ideal for borrowers who:

- Have unstable or unpredictable income

- Do not plan to refinance or sell the asset

- Are not financially disciplined or risk-tolerant

Final Thoughts

A balloon loan can be a smart short-term financing tool—but only when used strategically. The appeal of lower monthly payments comes with the responsibility of preparing for a significant lump-sum payment at the end of the term. It is critical to fully understand the structure of the loan, your repayment options, and your exit strategy before signing on the dotted line.