When you take out a loan—whether it’s for a car, a home, education, or personal use—one of the most important documents you’ll receive is the loan repayment schedule. This schedule outlines how and when you’ll repay the money you borrowed, along with the interest it accrues. Unfortunately, many borrowers overlook this document, only to be caught off guard by due dates, payment amounts, or interest calculations later on.

In this comprehensive guide, we’ll break down what a loan repayment schedule is, how it works, the different types you may encounter, and how to use it to manage your finances more effectively.

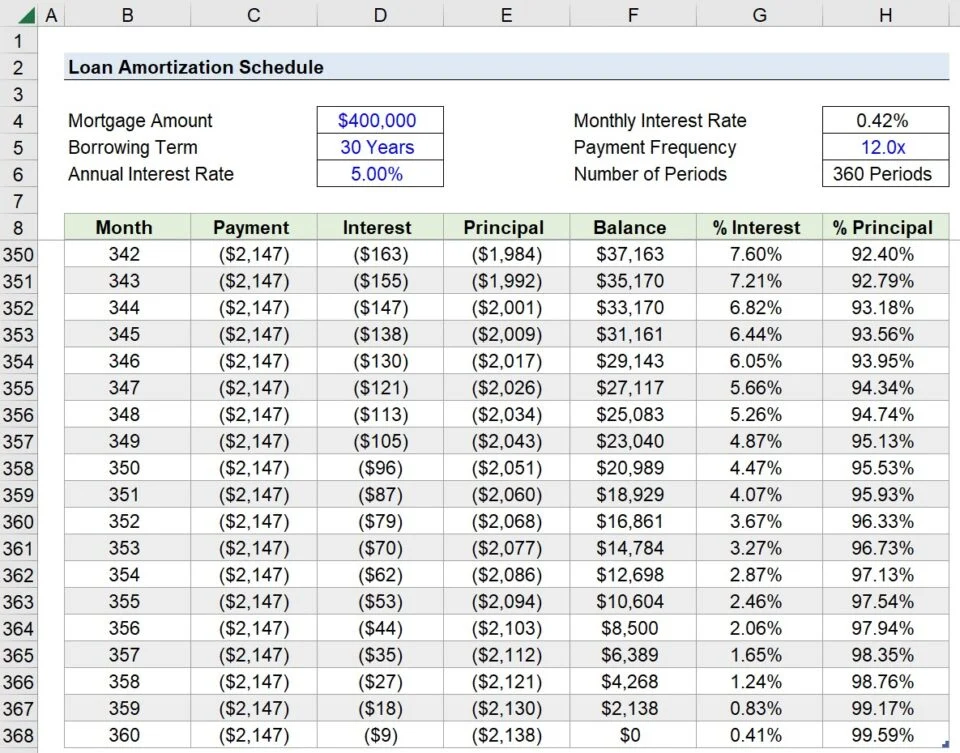

What Is a Loan Repayment Schedule?

A loan repayment schedule is a detailed breakdown of your loan repayment structure. It shows:

- Each payment amount

- Due dates

- How much of each payment goes toward interest and principal

- The remaining balance after each payment

It’s essentially a roadmap of your repayment journey from the day the loan begins to the day it’s fully paid off.

Why Understanding Your Repayment Schedule Matters

Understanding your repayment schedule is essential because it helps you:

- Plan your monthly budget

- Avoid late or missed payments

- Track how quickly your principal is being paid down

- Minimize interest costs by identifying opportunities to pay early

- Avoid penalties and loan defaults

Key Components of a Loan Repayment Schedule

Here’s what you’ll typically see in a repayment schedule:

1. Payment Number

Each payment is numbered sequentially (e.g., Payment 1 through Payment 60 for a 5-year loan).

2. Due Date

The date by which the payment must be made.

3. Payment Amount

The total monthly payment, usually fixed for most installment loans.

4. Interest Portion

How much of the payment goes toward interest.

5. Principal Portion

How much of the payment goes toward reducing your loan balance.

6. Remaining Balance

The outstanding loan amount after each payment.

Types of Loan Repayment Schedules

There are several kinds of repayment schedules, depending on the loan type and lender terms.

1. Fully Amortizing Schedule

- Most common

- Each payment covers both interest and a portion of the principal

- Loan is fully paid off by the end of the term

2. Interest-Only Schedule

- Payments only cover interest for a set period

- Principal is repaid later—often as a lump sum

- Common in some mortgages and balloon loans

3. Balloon Payment Schedule

- Lower monthly payments for a set term

- Ends with a large lump-sum payment (the balloon)

- Used in short-term or real estate loans

4. Graduated Repayment Schedule

- Payments start low and increase over time

- Often used in student loan repayment plans

- Useful for borrowers who expect their income to grow

How Loan Repayment Schedules Are Calculated

Repayment schedules are based on:

- Loan amount

- Interest rate (fixed or variable)

- Loan term (length)

- Payment frequency (monthly, bi-weekly, etc.)

The most common formula for fully amortizing loans is:

Monthly Payment = [P × r(1 + r)^n] / [(1 + r)^n – 1]

Where:

- P = Principal

- r = Monthly interest rate

- n = Number of payments

Modern lenders typically generate your schedule automatically, but it’s important to understand how the math works behind the scenes.

How to Access Your Repayment Schedule

You can find your repayment schedule in:

- Your loan agreement

- Your online account with the lender

- Monthly billing statements

- Or you can generate one using loan calculator tools online

If you can’t locate it, contact your lender and request a copy. Every borrower is entitled to a clear breakdown of their repayment structure.

How to Read and Use Your Repayment Schedule

Here’s how to interpret and leverage the schedule to your benefit:

1. Budgeting and Financial Planning

By knowing your exact monthly payment, you can set aside funds in advance and avoid financial surprises.

2. Identifying Interest vs. Principal

Early in the loan term, a larger portion of your payment goes toward interest. Over time, more of it goes toward principal. This knowledge can help you make additional payments that target the principal and reduce your total interest.

3. Tracking Your Progress

Watching your loan balance decrease with each payment can be motivating. It also allows you to stay on schedule or even pay off your loan early.

4. Avoiding Penalties

Some loans carry prepayment penalties or fees for late payments. Understanding when and how to pay helps you avoid unnecessary charges.

Benefits of Making Extra Payments

Even if you follow your repayment schedule perfectly, there’s value in paying extra when possible. Here’s how:

- Reduce your loan term significantly

- Save on interest costs

- Build equity faster (in the case of mortgages or auto loans)

- Boost your credit score by lowering outstanding debt

Just make sure to confirm with your lender that extra payments are applied to principal and not future interest.

Common Mistakes to Avoid

When it comes to managing your repayment schedule, avoid these errors:

- Ignoring interest rates and assuming payments go mostly to principal

- Missing due dates, which leads to late fees or credit score damage

- Not checking for prepayment penalties

- Failing to update your schedule after refinancing or modifying loan terms

Tips for Staying on Top of Your Repayment Schedule

- Set up automatic payments to avoid missed deadlines

- Create payment reminders using apps or calendars

- Review your loan balance quarterly

- Use financial management tools to visualize repayment progress

- Contact your lender immediately if you can’t make a payment

What Happens If You Miss a Scheduled Payment?

Missing a loan payment can lead to:

- Late fees

- Damage to your credit score

- Default status if payments are missed for 60–90 days

- Collection activity

- Legal consequences in severe cases

Always communicate with your lender. Many offer grace periods, deferment, or hardship plans to help you stay on track.

Conclusion: Take Control of Your Loan Repayment

Understanding your loan repayment schedule puts you in control of your financial future. It enables smarter budgeting, protects your credit, and can save you thousands in interest. Whether you’re just starting your loan journey or already deep into repayment, regularly reviewing your schedule keeps you focused, informed, and financially responsible.